WELCOME TO PHUKET ISLAND UNITED KINGDOM OF THAILAND

Phuket Visa Law Office provides many range of legal services to private and cooperate clients across Thais and foreigners to better service needs in administration of resident visa or temporary visa, accounting and social security insurance. In addition to serving our clients directly, our lawyers serve as experts in English and Thai laws or both litigation matters.

The firm offers its clients all the legal, tax and accounting services required to conduct business in Thailand effectively. Over the years, the firm has advised in the areas of setting up businesses, company formation, notary public, all type of visa such as retirement visa, marriage visa, visa base on supporting Thai citizen, tourist visa and student visa. The firm can provide visa run to the consular section in Penang or to Ranong Border if needed.

You can visit our office in person, by telephone, fax or by email. Please do not hesitate to contact us and we can offer preliminary legal advice for free of charge which will be more or less advantage for you in the near future.

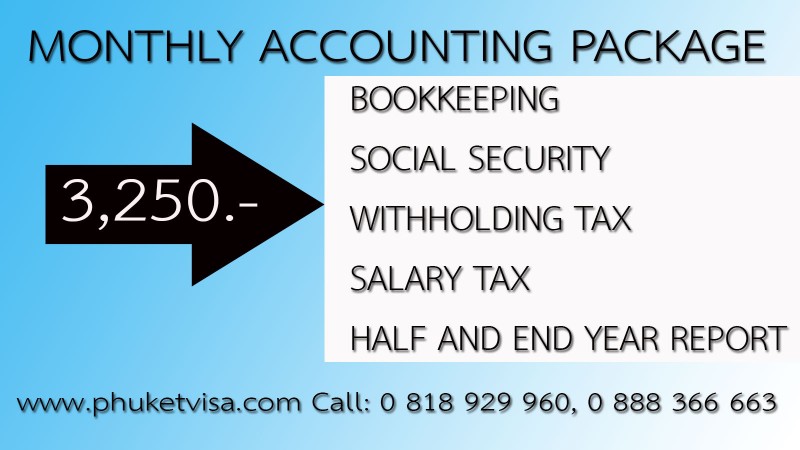

We are a service office accounting service Filing a tax return filing social security Juristic Person Registration Service Registration of various licenses and legal consulting services and document certification of all kinds. including business visa services final visa Marriage visa for Thai people Thai sponsor visa tourist visa student visa There is also a service to take you to apply for a visa to the Consulate of Penang. in malaysia and take you to a visa run in Ranong next to Myanmar

We have our own office, you can come to us or you can telephone, fax and e-mail. Contact us anytime or even if you are not our customer We are happy to give advice free of charge. Do not hesitate to contact us to alleviate any problems you think you don't know who to consult or are worried about the expense of contacting us. We invite you to come in. We are happy to serve you. You can suggest channels that are beneficial to you.